How can we help you?

How can we help you?

How can we help you?

Start Your

Journey

Journey

Fine-Tune Your

Future

Future

Thrive in

Retirement

Retirement

Independent, fee-based fiduciary advisors specializing in retirement planning, tax strategies, charitable gifting, and multi-generational wealth management. Our collaborative team, including CFP® Professionals and in-house tax professionals, helps individuals, families, and employers design their best retirement.

We work with employers to help provide customized retirement plan solutions for their employees.

Providing answers to design your best retirement

Subscribe for Weekly financial insights.

Years in business

(Founded in 1976).

Clients by household.

Employees across

two locations.

Assets under management

(in millions).

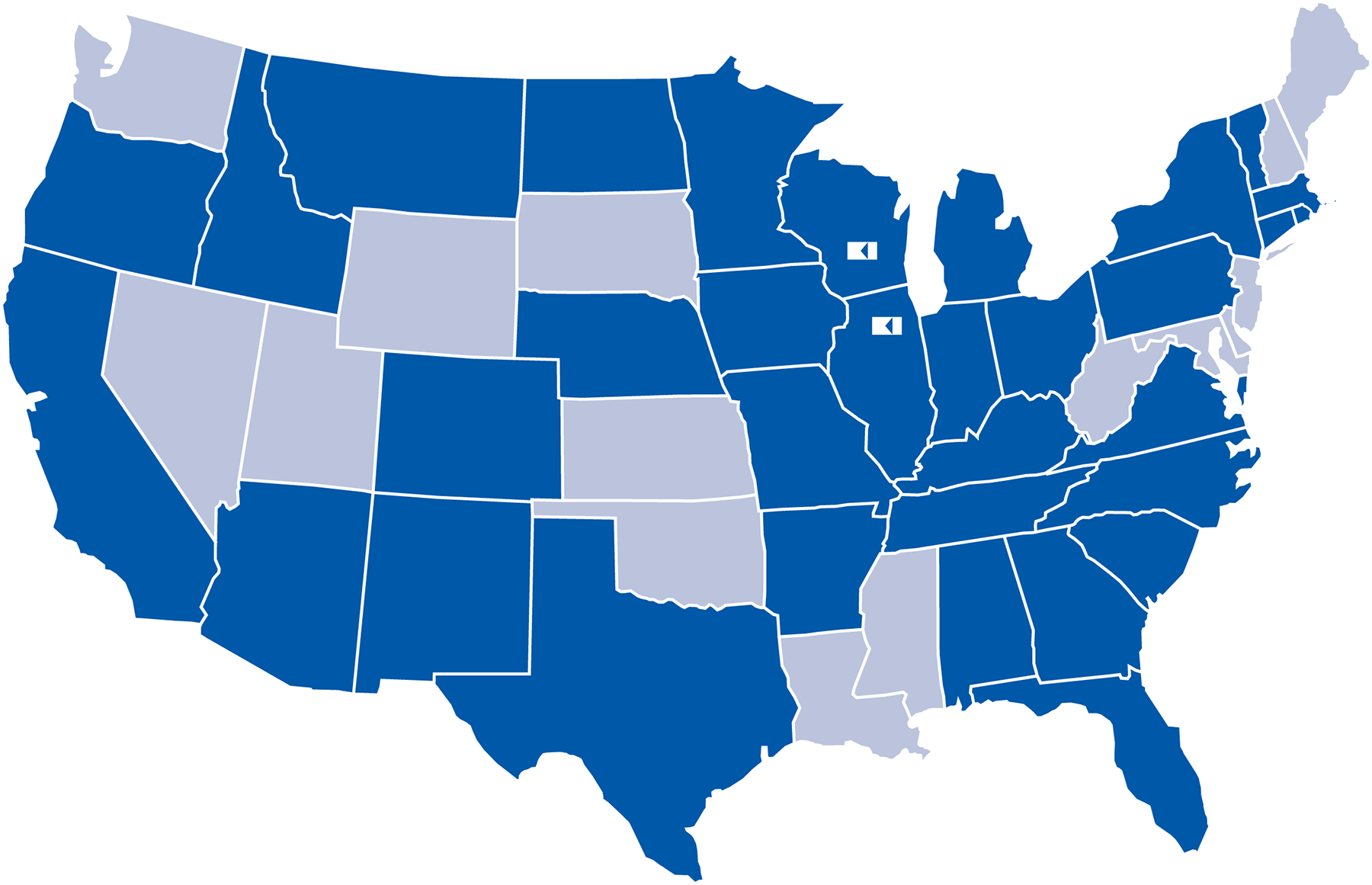

States where clients

are served.

This total represents approximately $771 million in client assets under management through our discretionary asset management wrap fee program (Klaas Investment Portfolios – KIP), approximately $8 million in retirement plan assets through our Klaas 401K Retirement Plan Services discretionary 3(38) offering, approximately $27 million in assets under advisement through our Klaas 401K Retirement Plan Services non-discretionary 3(21) offering, and approximately $27 million in assets under advisement through our non-discretionary Klaas Investment Consulting Services for brokerage customers. All "By the Numbers" data is as of April 1st, 2026. **We proudly serve clients in 34 states with two offices located in Wisconsin and Illinois.

![]()

![]()

![]()

© Copyright 2007-2026 Klaas Financial Asset Advisors, LLC All Rights Reserved. Klaas Financial Asset Advisors, LLC is a registered investment adviser registered with the United States Securities and Exchange Commission. Please click here for a list of our full Site Disclosures.

4707 Perry Ridge Lane

Loves Park, IL 61111

Monday-Thursday: 8am-5pm

Friday: 8am-3pm

Additional hours by

appointment only

5951 McKee Road, Suite 200

Fitchburg, WI 53719

Monday-Thursday:

8am-5pm

Friday: 8am-3pm

Closed daily for lunch

(12pm-12:30pm)

Additional hours by

appointment only